Petrochemicals: Mar 30-Apr 3: Rise in prices yet to be passed on to downstream market

[Aromatics]

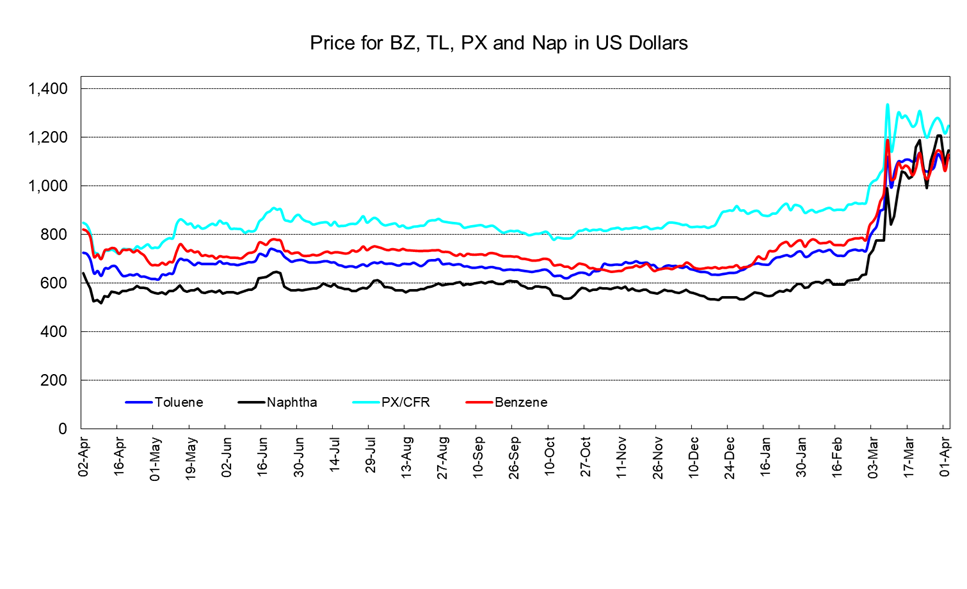

Benzene prices on an FOB Korea basis and paraxylene (PX) prices on a CFR Northeast Asia basis were still at high levels along with prices for benchmark feedstock crude oil and naphtha. Since a rise in costs was slowly passed on to prices of downstream products, the upper end of the benzene and PX market was occasionally pressured.

[Olefins]

Ethylene prices on a CFR Northeast Asia basis were bullish. As more naphtha crackers were shut down or operation rates were reduced due to shortage of naphtha, supply was tight. In China, since profitability of derivatives was worsening, some players reduced production of derivatives and sold ethylene. Under this situation, prices fluctuated at high levels. Regarding facilities, Taiwan's Formosa Petrochemical shut down its naphtha cracker for production adjustment.

Propylene prices on a CFR Northeast Asia basis softened. End-users finished purchase of April delivery cargoes and buying interest receded. Production volumes were expected to decrease going forward along with turnaround of propylene facilities. For this reason, buying interest from end-users might rise after discussions for May cargoes started. On the other hand, CFR Southeast Asia prices increased due to tight supply. For delivery to Indonesia, an April cargo was traded at $1,500/mt.

In the butadiene market on a CFR Northeast Asia basis, prices were seen to have hit the ceiling. Due to a previous hike in prices, profitability of derivatives was seen to have worsened. Buying interest for butadiene receded slightly. A cargo loading in China in May was reportedly traded for delivery to South Korea.