Petrochemicals: Jun 8-12: Propylene softens amid ample supply

[Aromatics]

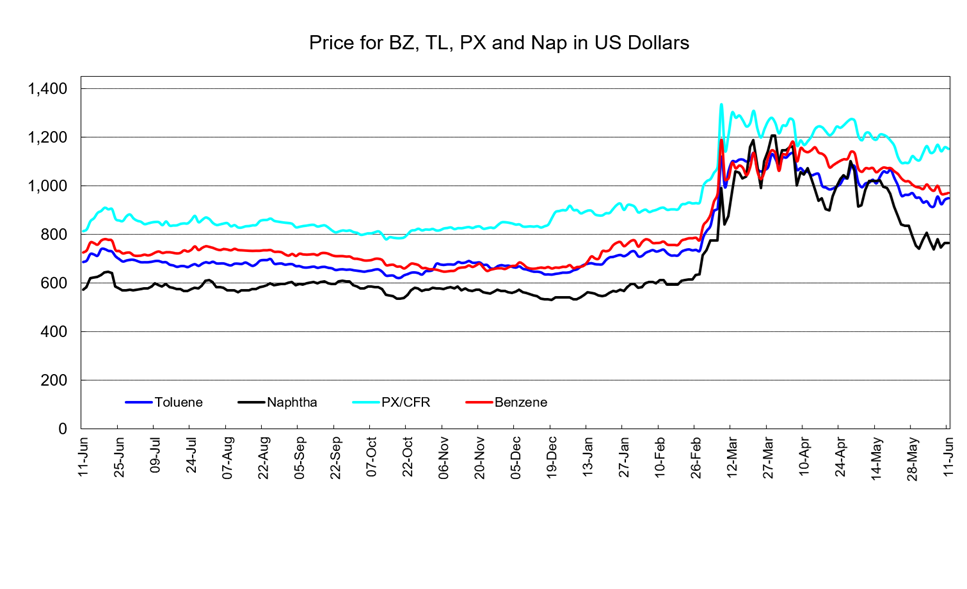

Benzene prices on an FOB Korea basis and paraxylene (PX) prices on a CFR Northeast Asia basis softened slightly towards the end of the week compared to the beginning. However, compared to benchmark feedstock crude oil and naphtha price, price spreads remained intact. The Northern Hemisphere entering the summer driving season was cited as a bullish factor.

[Olefins]

Ethylene prices on a CFR Northeast Asia basis were soft. For CFR Southeast Asia, a deal was reported in the low $900's/mt for a July arrival cargo. Due to sluggish demand for polyvinyl chloride (PVC), a derivative, operational rates at PVC facilities in China declined, which led to a drop in ethylene demand. South Korean petrochemical makers, in the wake of deteriorating ethylene margins, further lowered their naphtha cracker operating rates; however, the ethylene surplus across Asia could not be fully absorbed.

The Asia propylene market saw widespread declines on a sense of ample supply. In the CFR Northeast Asia market, with offers seen from South Korea, Taiwan, and Southeast Asia, supply was perceived to be ample. Meanwhile, buying interest from end-users remained weak. Under these circumstances, market sentiments were weak. In Taiwan, Formosa Petrochemical (FPCC) issued a sell tender for July loading. In the Southeast Asian market, petrochemical makers in Malaysia and Vietnam had room to sell.

Butadiene prices on a CFR Northeast Asia basis were soft in the wake of weak buying interest. With production cuts of derivatives, butadiene demand appeared to be retreating. Looking ahead to the summer, some market participants held views that demand for tires would decline. The spread between buyers' and sellers' ideas was wide, and trade activity was not active.

To view sample report, click on icon below